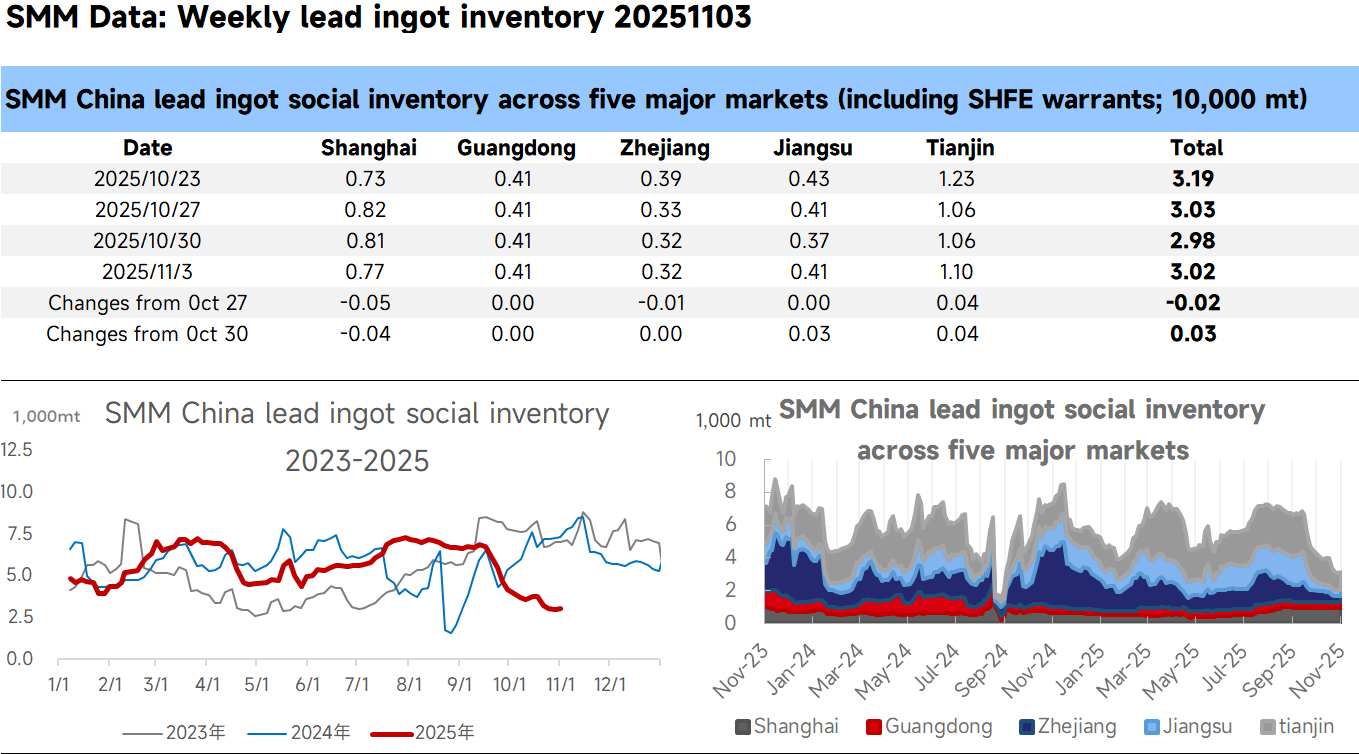

In November, maintenance and production resumptions occurred simultaneously among primary lead and secondary lead enterprises. Some delivery brand enterprises specializing in primary lead are currently undergoing maintenance, while secondary lead smelters in Anhui have gradually resumed production, driving an overall upward trend in supply. Meanwhile, as the SHFE lead 2511 contract approaches delivery, some suppliers intend to ship to delivery warehouses, leading to a transfer of a certain volume of lead ingot inventory. This has caused the social inventory of lead ingots to stop falling and rebound. Additionally, before the delivery is completed, there remains the possibility of invisible inventory transforming into visible inventory. Coupled with expectations of increased production from domestic smelters resuming operations and the arrival of imported lead, the social inventory of lead ingots is expected to have further room for growth.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM’s internal database model. The data are for reference only and do not constitute decision-making advice.